Credit, Collections & Insolvency News

PwC’s Consumer Sentiment Index for March 2022 has seen a considerable drop off in sentiment reflecting the cost of living crisis.

The Index found that consumer sentiment is currently tracking at -20, after peaking at +10 in June 2021. A 30 point decline in nine months is the biggest sustained fall in the survey since the global financial crisis in 2008. However, at -20, consumer sentiment is still higher than it was at the start of the pandemic (-26), after Lehman’s collapse in Oct 2008 (-51) and the post-recession austerity period (-42).

This time last year, the Index measured +8, driven by improvements across every age group and demographic. At that point we saw an upturn in category spending intentions, with more discretionary purchases linked to leisure, recreation and fashion prioritised over groceries and the home.

Run across the weekend of 17-20th March, the latest survey shows the real impact of the cost of living crisis across the UK, with the findings coming after the start of the conflict in Ukraine, but before the Chancellor’s Spring Statement.

Historically, there have been relatively consistent patterns in sentiment between different demographic groups. Young people, for example, are more optimistic – typically due to entering the workforce and progressing their careers – unlike older people whose income has typically plateaued or are closer to exiting employment.

The latest index shows that whilst sentiment has fallen in almost every age group, the gap between the most and least optimistic is wider than ever. Worries over inflation and disposable income are weighing on consumer’s minds. Albeit the younger age groups see inflation as least likely to affect them, but this could be due to more younger people still living at home.

Last March’s sentiment tracking saw category spending expectations much improved, as the prospect of lockdown easing and for the first time in the history of the index, discretionary categories exceeded the more ordinary, such as grocery shopping, for example.

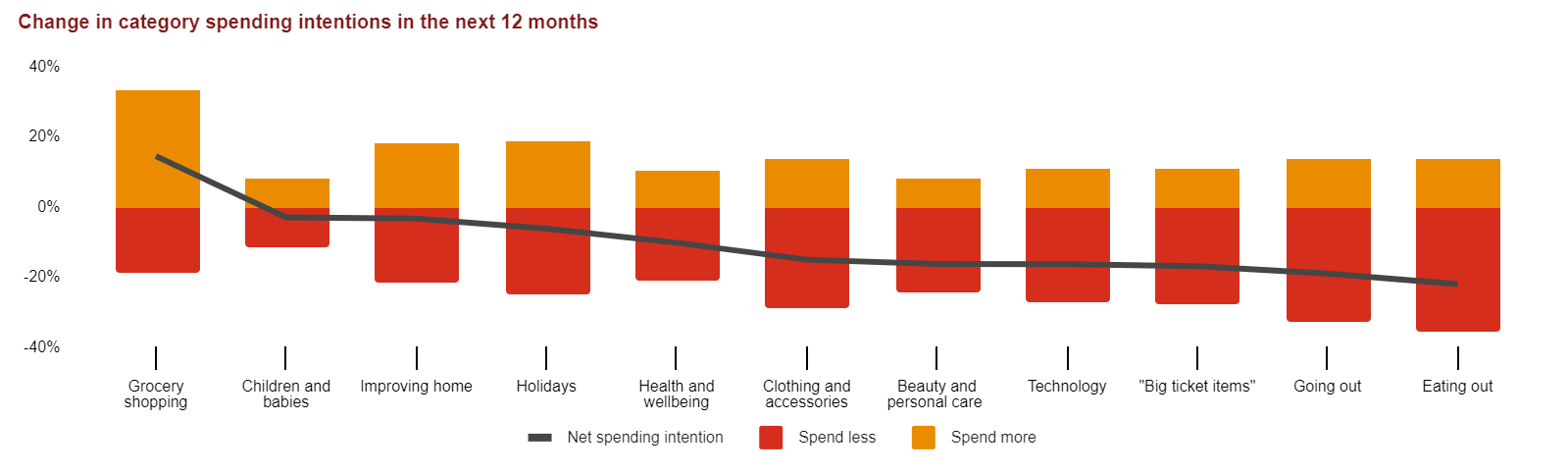

However, the latest index shows a complete reversal in consumer priorities. Grocery shopping is the only category with a net positive spending intention, where people expect to spend more, rather than less in the next 12 months. This will almost exclusively be driven by inflation, rather than specifically heightened consumer demand.

Elsewhere, spending expectations on going and eating out have significantly dropped, with both categories now the lowest. Holidays and fashion spending have also seen substantial falls since last Spring. While pent-up demand and weak comparatives mean that both of these categories should see double digit growth vs 2021, neither are expected to approach pre-pandemic heights, given the impact of the wider cost-of-living crisis on disposable income.

Lisa Hooker, Consumer Markets Leader at PwC, said “It’s clear that consumers are having to deal with a significant change in their spending priorities compared to even a year ago, where the index measured a record level of positive sentiment coupled with spending intentions ramping up in more discretionary categories such as leisure and fashion. With the latest research, we see consumer spending expectations move almost exclusively toward more vital and essential areas such as grocery shopping, children and babies.”

“The shift in sentiment is both significant and sudden. Whilst there is still some post-Covid recovery, spending expectations on eating out and going out have plummeted as consumers look to tighten their belt as they face up to cost of living pressures. Even after the extensive travel disruption over the last two years, holiday spending is not immune and will consumers prioritise their main holiday over other breaks, like we saw during the global financial crisis?”

“Businesses that can help their customers to cope with the crisis by offering them the choice to trade down – whether special offers, cheaper brands, or set menus, for instance – are more likely to keep their loyalty for when things get better.”