Latest figures from UK Finance have shown that there has been a decline in mortgage lending, with lending for house purchases down 28% year-on-year in Quarter 2 (Q2).

UK Finance says that the levels of housing market activity have remained very low by comparison with recent years in the first half of 2023. The industry body said this was driven by the “significantly greater affordability challenges currently faced by borrowers,” with rising interest rates delivering a hike in the cost of mortgages. The report shows that record numbers of borrowers chose to refinance with their existing providers, with 84% of remortgaging deals internal transfers. This compares to an average of 77% across 2022. UK Finance data also shows that consumers are seeking out better deals for their savings. Deposits in easy access accounts fell by 7% year-on-year, while deposits in notice accounts, which offer higher interest rates, grew by 23%. Household deposits continued to fall following the slight drop in Q1.

Lending for house purchases and external remortgaging remained weak in Q2 2023, impacted by affordability constraints and a reduction in house buying and selling activity. The trend of increased borrowing over a longer term to stretch affordability looks to have reached its limit.

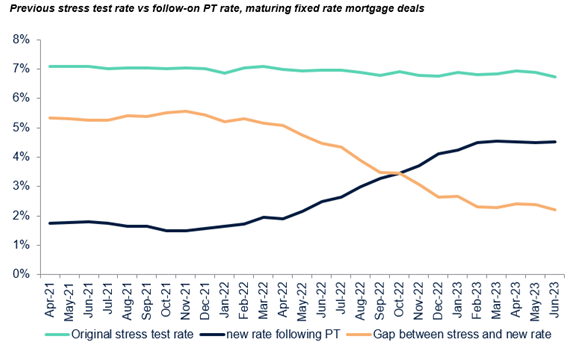

The analysis shows mortgage borrowers who have refinanced internally at the end of a fixed-rate deal are doing so within the stress-test level applied to their original application.

Lenders continue to provide support to any customer struggling with their finances and have recently enhanced customers’ options through the Mortgage Charter. Households continued to dip into their savings in Q2, although there was also a shift towards notice accounts which generally offer a higher return.

Borrowing for house purchases saw a sharp fall at the start of the year and this continued in Q2 with activity down nearly a third compared with the same period in 2022. First-time buyer purchases and homemover purchases were down 28 per cent and 30 per cent respectively in Q2 2023 compared to the same period the year before.

This is largely due to uncertainty in the market as well as affordability issues: house prices relative to income are near historic highs, which combined with higher interest rates and increased costs of living, means it has been harder for some borrowers to meet regulatory affordability tests.

Throughout 2022 we saw a rapid increase in the proportion of mortgage customers borrowing over a longer term in order to stretch their affordability. However, the levelling off of this trend in Q1 continued in Q2. We also saw typical income multiples and average loan-to-values start to fall back, favouring those with higher incomes and/or larger deposits.

Affordability constraints impacted some external remortgaging activity and resulted in internal product transfers being more popular. The second quarter saw 84 percent of remortgaging deals being internal product transfers and within that, April was a record monthly high at 88 per cent – by comparison the average for 2022 as a whole was around 77 per cent.

UK Finance has conducted analysis on borrowers that refinanced internally this year, looking at their new rate compared to the rates they were assessed against for affordability purposes when they previously took out their mortgage.

This is set out in the graph below and shows that while people are now paying materially higher rates, these rates are below the prior stress test rate. Therefore, while there are significant pressures on household finances at the moment, customers will typically retain a decent level of wiggle room in their budgets after refinancing.

It also shows that the underwriting standards operated by the mortgage industry and enshrined in FCA rules since 2014 are doing the job they were designed for, ensuring customers’ finances are resilient against even the significant payment shock many are now seeing.

Mortgage arrears rose in line with expectations, although the total level of arrears remains low by historic standards. Lenders continue to work with their customers who experience financial difficulty to provide tailored forbearance that best meets each customer’s circumstances.

Consumer spending meanwhil increased in Q2 in line with consumer confidence. While some of the increase can be attributed to price rises, there does appear to remain an underlying willingness and ability of people to spend. This is likely to be supported by the savings buffer many households built up during the pandemic.

Borrowing through personal loans totalled £4.7 billion, up slightly from £4.6 billion the previous quarter.

The rate of growth in outstanding credit card balances appears to have levelled off. Credit card debt is around 11 per cent below its pre-pandemic peak while the average spend has increased due to inflation. The proportion of interest-bearing credit card debt continued to fall, indicating that households are largely able to pay off their balances each month.

Eric Leenders, Managing Director of Personal Finance at UK Finance, said “Whilst the cost of living challenges have created acute hardship for many, we have also seen that other consumers were largely able to pay off their credit card bills and meet their monthly mortgage payments. Some have been dipping into their savings to help to pay the bills, whereas some of those with savings have moved their money to accounts with higher rates to maximise their income.”

“Around 700,000 borrowers have come off their fixed rate deal in the first half of this year and likely found themselves on a much higher rate, which continue to be largely affordable because of the “stress tests” applied when the mortgage was originally taken out. But circumstances can change, so if anyone is struggling with their mortgage payments, they should reach out to their lender who will have a range of tailored support available to help.”