Amid challenging times for the UK economy, UK Finance expects the cost of living pressures and rising interest rates to reduce demand for house purchases between 2023 – 2024.

The number of property transactions to fall 21 per cent next year (from around 1.2 million in 2022 to 1 million in 2023), with the value of lending to homeowners dropping 23 per cent, and lending to landlords falling 27 per cent. Despite the anticipated fall in activity, the UK has a strong mortgage and housing market which will remain competitive.

At the same time, it is expected that there will be a strong demand for refinancing as around 1.8 million fixed rate mortgage deals are scheduled to end in 2023.

Affordability pressures facing borrowers will mean some borrowers, particularly amongst lower income brackets, may find remortgaging options more limited on the open market. However, with widespread availability of internal product transfers, we expect refinancing overall to be strong through next year. It is expected that will be around £212 billion of product transfers to take place next year, compared with an estimated £197 billion in 2022.

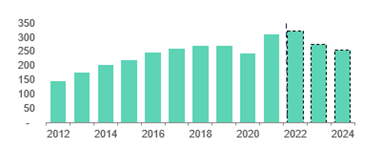

Gross mortgage lending, £ billions

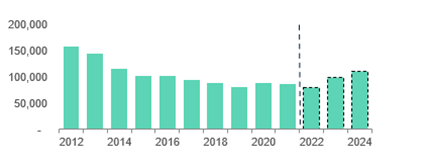

However, any rise in unemployment, coupled with cost of living pressures and interest rate increases, will put further pressure on some households. We expect this pressure will begin to show in rising mortgage arrears from early 2023, increasing through the year and into 2024. We anticipate the number of households in arrears to reach 98,500 next year, representing around one per cent of outstanding mortgages. By historic standards these increases arrears figures do remain low.

Possessions numbers rose modestly during 2022 as lenders and the courts worked through the backlog of cases that had built up due to the pandemic induced possessions moratoriums. As historic cases make their way through the courts the number of possession cases has risen and we expect this to continue slowly through the next two years as the backlog is cleared. However, as noted above with arrears the increase in the number of properties being repossessed remains low compared to the years prior to the Covid-19 pandemic.

However, with arrears currently still low and with few new arrears cases emerging to date, we do not expect material numbers of possessions related either Covid-19 or the current headwinds facing household finances until well into 2024.

It is important to note that possession is only ever a last resort and taken when all other forms of support have been explored with the borrower. Support is available to all customers who might be struggling with their mortgage payments. We would encourage borrowers to get in touch with their lender early to discuss the tailored options available for their particular circumstances.

First charge mortgage arrears

Commenting on the data John Phillips, National Operations Director at Just Mortgages said ”As i read through the Mortgage Market forecast for 2023 from UK Finance there was a certain amount of pessimism with a prediction of overall mortgage lending dropping by 15% and overall property transactions falling by 21% next year. However, remortgage activity is predicted to increase in 2023 and lending is expected to return to pre-covid levels says UK Finance.”

“2023 will, without question be a year for brokers to be proactive and it will very much be a case of getting out what you put in.”

“Mortgage brokers have dealt with far worse economic environments and come out the other side. We need to help borrowers accept that rates of four and five percent are the new normal and household budgets should be adjusted accordingly. Brokers are in a very privileged position to be able to help people buy or keep their homes and good products still exist and let’s remember that lenders still want to lend.”

“Diversification will be the watch word for brokers in 2023 and they should look to become proactive in all lending sectors even those they have not targeted previously such as equity release, commercial and overseas mortgages. There is also an untapped income for many brokers by simply ensuring that their existing and new clients have the appropriate protection needs met.”

“There is also the opportunity to ensure that borrows wider financial circumstances are looked after with a referral to a pensions or wealth expert where the , there is so much better if a fee can also be earned from a terrific referral.”

“2023 can be a year of opportunity for brokers; they just need to seize it.”