Credit, Collections & Insolvency News

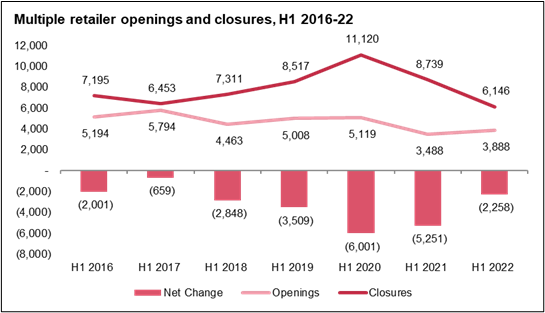

Store closures by multiple retail operators have stabilised to the lowest rate in over seven years but openings have yet to recover to pre-pandemic highs, suggesting retailers are exercising strict caution in the current trading environment according to PwC’s latest Store Openings and Closures report for H1 2022.

Closures have seen an accelerating trend since the mid 2010s, driven primarily by the shift to online retail and services such as banking and post offices. However, this was offset to some extent due to the rapid rollout of leisure operators, such as casual dining restaurant chains and coffee shops.

We saw a rapid shake out during the pandemic (2020 and 2021), predominantly affecting retailers who had overexpanded, such as restaurant chains, and those which had not adapted their operating models to omnichannel – notably fashion.

In the current landscape, the shake out has now happened, meaning a sharp deceleration in closures by almost half compared to the pandemic at its peak (34 closures per day H1 2022 vs 61 closures per day H1 2020). Openings, on the other hand, have stabilised but are yet to start showing signs of any notable increase (21 openings per day in H1 2022 vs 32 per day at its peak in H1 2017).

The spread of closures between regions are also at their lowest for over seven years – with the East of England and the West Midlands at -1.4% compared to the North East and South East at 0.8%, showing a reversal in the trend of the last two years of higher closures in more urban areas. London in particular, which saw -3.3% net closures in H1 2020 and -2.9% in H1 2021, has seen net closures improve to -1.3% this year, as the trend to working from home has stabilised.

Leisure operators make up three of the four fastest growing categories in the report, each for varying reasons:

Takeaways have been boosted by the growth of home delivery, which has made stores more viable. Additionally, strong, branded chains are often franchises – which can be owned and operated by local entrepreneurs. Complimented by the ability to operate throughout lockdowns and the pandemic, there are strong brands meeting emerging consumer needs – which are ripe for growth.

Restaurants have been one of the worst performers in the past three years. While administrations and restructurings closed many branches of large chains en masse, new chains have been able to expand quickly into empty spaces and take advantage of lower rents and pent-up demand post-lockdown.

Amusement arcades have taken advantage of vacant units and lower rents to open particularly in suburban areas and seaside towns.

While not categorised as leisure, DIY shops, including trade counters, have taken advantage of home improvement trends formed during lockdowns

This year’s report sees only four categories seeing a 100+ net decline in units.

Banks and financial services (199 net closures) have featured in the top 10 fastest declining outlets for the past seven years, except in 2020, when they were eclipsed by other retail categories at the outset of the pandemic. Longer term withdrawal of physical branches, combined with the shift to online banking and digital services is likely to see this trend continue.

Historically, charity shops (199 net closures) have been able to expand into vacant retail space. But this is contrasted with two issues which they have been unable to avoid: the shift online for shopping and emerging digital marketplaces for pre-loved items; and staffing issues due to a typical reliance on older volunteers.

For betting shops (226 net closures) and fashion retailers (128 net closures), their closure rate has improved significantly compared with previous years: H1 2021 saw 1,063 fashion retailers closed, driven by multiple high-profile administrations during the pandemic; while 862 betting shops closed in H1 2020, primarily driven by legislative changes.

Lisa Hooker, Industry Leader for Consumer Markets at PwC UK said

“A reduction in closures and growth in openings give some reason for optimism, but any positivity must also be viewed alongside the significant concerns over the rising cost of living and how it will impact people’s ability to spend. In addition to pressures on consumer demand, we mustn’t also forget that increasing utility, input and labour costs will significantly affect the viability of all high street businesses.

“While the outlook is better than it was during the height of the pandemic, it’s worth noting that the numbers still show a decline, with our net numbers equating to 12 closures a day in the first half of this year. Added to that, retail footfall remains 10-15% below pre-pandemic levels and openings lack momentum – particularly outside leisure.

“With soaring prices for food, petrol and utility bills, inflation at a 40-year high and the Bank of England warning the UK will fall into a prolonged recession at the end of this year – this will impact everyone, and is only expected to deepen. We’ve already seen it impact Consumer Sentiment this year, and retailers and operators must help consumers mitigate their financial challenges now, while protecting themselves from the financial squeeze.

“While shopping behaviours have changed, the high street has stood the test of time, with a post-pandemic bounce back and our research indicating that the younger generation has more affinity with shops than perhaps expected. But it remains in a state of transition, and cosmetic interventions alone will not succeed. Success is also likely to depend on the focus of a new Prime Minister, and how they intend to help high streets. Business rates, for instance, will be a critical area for operators, and it will depend on how they are reformed in the near future (if at all). To truly level up, the challenge for local leaders – working with businesses and communities – is to create places that work for all those who visit, live or work there.”

Lucy Stainton, Commercial Director at The Local Data Company, said “This latest data tells a story of continued recovery, with the gap between openings and closures the smallest it’s been since the first half of 2017 – despite the end of Government support packages in March, supply-side issues due to the ongoing war in Ukraine and rising fuel prices.”

“The number of empty units across high streets, shopping centres and retail parks continues to decline, as we see the holes left behind from a litany of CVAs and insolvencies being either reoccupied or repurposed due to the new planning laws on converting retail property to other uses. As it stands, 25% of the former Arcadia portfolio, as an example, now has trading businesses occupying that space, with a further 6% being redeveloped for other uses to date. Whilst the latest numbers show an uptick in new openings as surviving operators return to growth mode, underneath the top-line statistics the trends are hugely varied. Although it has been over two years since the start of the pandemic, we are still yet to define our ‘new normal’ which is having a sustained impact on city centre locations with many new openings being focussed on smaller market towns and local high streets as people continue to work from home, with city centres further hampered by both train strikes and airport travel disruption reducing tourist numbers.

“What’s clear from the latest numbers, is that the impact of Covid-19 has finally washed through. However, we now face a new round of economic headwinds, so it remains to be seen if we can really expect this more positive trajectory to continue. That being said, surviving operators have learned huge lessons over the last couple of years and are well versed in the need to remain agile – so as an industry, we are better placed to survive these economic shocks and market challenges.”