Credit, Collections & Insolvency News

Credit Connect Media hosted the return of its Commercial Credit & Collections Conference last week at the Met Hotel in Leeds which saw trade credit, insolvency, and economic change and discussed by fourteen leading credit, collections and insolvency professionals.

In the sixth edition of the Commercial Credit & Collections Conference series, hosted by Credit Connect Media, industry professionals gathered to discuss the evolving strategies in commercial credit and collections. The forum examined in detail the impact of credit risk, insolvency, fraud and late payments.

Commenting on the event, speaker, Kulvir Ranu, Credit Manager at Lavazza Coffee said ”It was a great event. There was interesting insight across areas of concern; fraud, insurance and economics, and a great way to share knowledge. Thoroughly enjoyed the engaging discussions, and the unique perspectives of everyone present.”

Luke Sculthorp FCICM, Head of Strategic Relationships, Chartered Institute of Credit Management (CICM) said “The Credit Connect Conference provided an exceptional platform for addressing the critical issue of late payments, which continues to impact businesses across the UK. The insights shared and collaborative discussions were invaluable in highlighting the urgent need for stricter enforcement of payment codes and the adoption of technological solutions to mitigate credit risks. The conference also covered a range of topics including credit fraud management, business risks, and innovations in credit management technology. A must-attend for anyone in the credit management sector.”

Brian Lewis, Credit Manager, CPI EuroMix Mortars said “It was a very good interactive session which, judged by the questions posed, was thought-provoking. I look forward to the next event”

Mark Halstead Co-founder at Red Flag Alert said “It was great to get out and talk about one of my favourite data points – Fraud… it is very frustrating for both financial institutions and staff of companies involved as you are constantly second-guessing your actions. But the reality is the fraudsters currently have the upper hand, staff training, raising awareness on a constant basis, and identifying your customers more positively ie passport / driving lic on accounts will all help.”

Michael Locke MD from Prism 339 said “It was a pleasure to be able to address the audience at the CC&C Conference. A tightly run event with a great combination of speakers, giving updates on both regulation and best practice. A useful day of networking for anyone in the credit sector.”

Whilst attendee Philip King said “It was a great conference, which was well attended. The content covered a wide range of topics with some really useful insights and discussion.”

Colin White Founding Director at Credit Connect which hosted the event said “It was great to see such a great mix of commercial credit and collections professionals take part in the industry panel discussions. I look forward to continuing the conversation at the next face-to-face version of the event taking place on Thursday 7th November in Manchester.”

The event was supported by Marsh McLennan, PKF, Red Flag Atradius Collections, Experian and the CICM.

Brian Lewis, Credit Manager, CPI EuroMix Mortars (BL): HMRC, in some cases yes but it’s probably too late by then but others are recognising their own issues and taking steps to avoid legal action, Albeit slowly.

Kulvir Ranu, Credit Manager at Lavazza Coffee (KR): HMRC’s aggressive approach is increasing the payment plan requests as HMRC almost become the preferred creditor so Businesses want to settle their debt prior to other creditors if they want to continue trading.

KR: Insurers are playing a part in the economic problems by withdrawing insurance and reducing agreed limits without prior notice, causing businesses to make rash choice on credit lines offered and raising fear of Trading with the customer within the business environment.

BL: Insurers, in some cases yes but on most policies there is always an element of uninsured customers. It then comes to the insured risk appetite and at what level they will trade backed by a bad debt provision rather than a full cover insurance policy. A mixture of both may be a solution.

KR: The Interest rates not reducing is concerning, this is making less money available for Businesses/Customers to spend along with increased cost of living, high energy costs, so customers hold on to money longer instead of paying.

BL: The Outlook is one of slow growth determined by the willingness of developers of all levels accepting the increased cost of construction. Fair treatment of sub-contractors and suppliers is some way away. One other aspect is the question of prompt payment and certainly, main contractors need to sign up and adhere to the prompt payment code rather than seeking ways around it or worse still ignoring it.

ML: I believe history will look back on 2019-2024 as dominated by the turbulence caused by Brexit/covid/political turnover/Truss ‘fiscal event’/Ukraine disruption/the consequent inflation. The fiscal policies of governments to respond to these events has created the largest waves that people have had to navigate, and the insolvencies of companies impacted by loss of access to the single market/easy capital/footfall in cities with the rise of remote working accounts for much of the insolvency we see.

Mark Halstead Co-founder at Red Flag Alert (MH): Very few people recognise straightaway they have been conned, therefore the monies are often moved in the first hour or two and never seen again, so recoveries are low.

Martin Kirby, Head of Credit Risk & Collections, Calor Gas (MK): The success rate in recovering the proceeds from scams and fraud can vary significantly, largely depending on the type of fraud, the speed of detection, and the effectiveness of the recovery strategies employed. While exact statistics can be hard to pin down, several factors influence recovery success:

Despite these efforts, recovery rates can still be low due to various challenges, including the complexity of international fraud schemes, legal hurdles, and fraudsters’ sophistication. Industry estimates suggest that recovery rates can be as low as 10-20% of the total fraud losses, but proactive measures and robust fraud response strategies can improve these odds.

MH: The only way is to be open, discuss it internally, understand how it happened, put remedies in place, only then can you confidently speak publicly about it, but in doing so know you help others.

MK: Encouraging openness about being a victim of fraud is essential for fostering a culture of transparency and continuous improvement. Here are several strategies to promote openness:

MH: Absolutely any and all businesses, but for sure where high volume transactions take place, where you have High Value Goods and very mobile goods. The number one thing is Money, so any requests to change bank details should be treated with suspicion, very few companies change bank accounts.

MK: Business fraud can affect any sector, but specific industries tend to be more vulnerable due to their structure, the nature of their transactions, or the value of their assets. The sectors most impacted by business fraud include:

By understanding which sectors are most impacted, companies can tailor their fraud prevention and detection strategies to address the specific risks they face. This is how I see being proactive: Stop reacting to fraud and get on the front preventative foot. It is in everyone’s gift and an easy business case.

Luke Sculthorp FCICM, Head of Strategic Relationships, Chartered Institute of Credit Management (CICM) (LS): While the primary focus of credit professionals is often on securing timely payments for their own invoices, there is a growing recognition within the industry of the importance of monitoring and improving how businesses treat their suppliers, particularly small businesses. By advocating for faster payments to these suppliers, credit professionals can help foster stronger, more sustainable supply chains and contribute to the overall health of the business ecosystem.

LS: The new payment regulations are expected to have a significant impact on late payments by introducing stricter compliance requirements and potentially more severe penalties for non-compliance. These measures aim to encourage timely payments and reduce the prevalence of late payments, which can be particularly detrimental to smaller businesses. Credit professionals will need to stay informed about these regulations and adapt their practices to ensure compliance and mitigate risks.

LS: Indeed, one of the most effective motivators for ensuring prompt payment is fostering a culture where all businesses view their supply chain partners, both upstream and downstream, as integral collaborators. This partnership approach encourages mutual respect and understanding, leading to more timely payments and stronger, more resilient business relationships. By treating suppliers as partners, companies can enhance trust and reliability across the supply chain.

LS: The aggressive promotion of Supply Chain Finance (SCF) by banks can be seen as contradictory to the principles of the Prompt Payment Code (PPC), which emphasises prompt payment practices. While SCF can provide immediate liquidity to suppliers, it may inadvertently encourage buyers to delay payments, relying on the financing to bridge the gap. The industry needs to strike a balance where SCF is used to support cash flow without undermining the commitment to timely payments as advocated by the PPC.

LS: Making the Prompt Payment Code (PPC) mandatory for larger corporations, coupled with more stringent penalties for non-compliance, could significantly enhance its effectiveness in promoting timely payments. The threat of removal from the PPC alone may not be sufficient to deter late payments. Stronger enforcement mechanisms and greater accountability are essential to ensure that large corporations adhere to the standards set by the PPC, thereby improving payment practices across the industry.

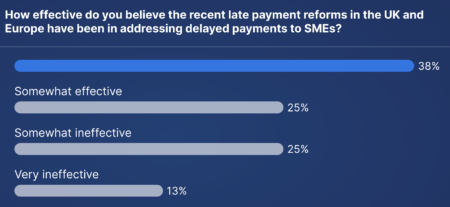

Selected Event Poll Results

![]()

*Data and statistics copyrighted to Credit Connect