A new report from the Pensions Policy Institute (PPI) has found that people hoping to enjoy a ‘moderate’ standard of living in retirement could need over a third more income,

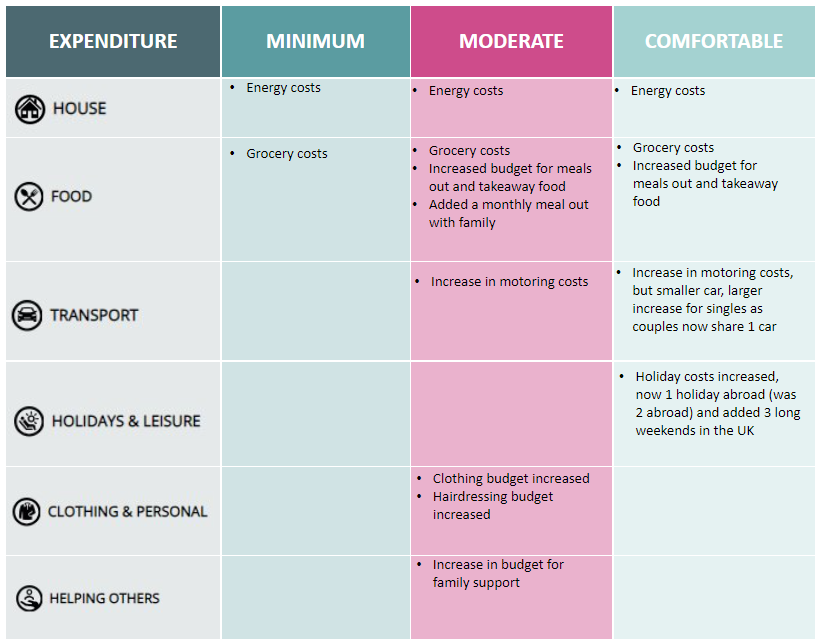

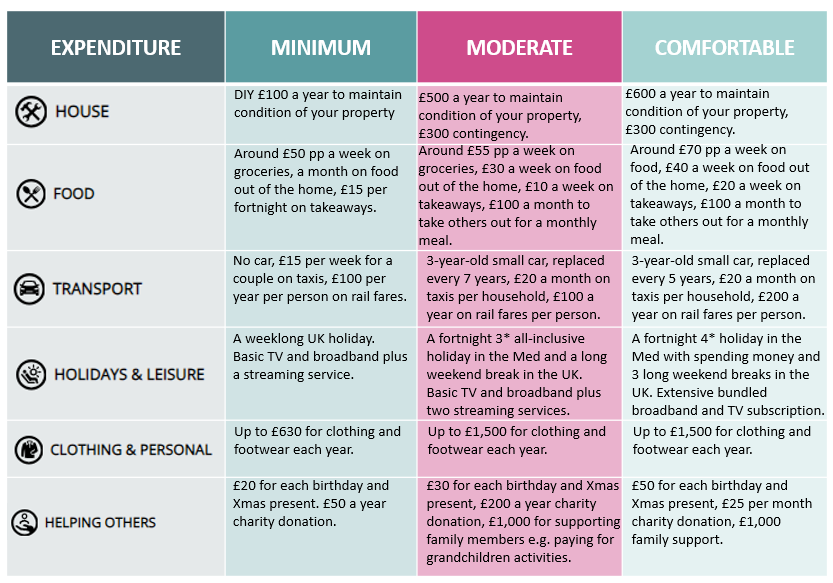

The latest update reveals that a moderate living standard in retirement could cost a single person £31,300 in 2023/24, up 34% from £23,300 a year earlier

The cost of a minimum retirement living standard has increased from £12,800 to £14,400 for a single person and from £19,900 to £22,400 for a couple, according to data from the Pensions and Lifetime Savings Association.

A single person wanting a ‘comfortable’ standard of living could need to spend £43,100 a year and £59,000 for a two-person household, up 15% from £37,300 in 2022/23

A ‘minimum’ retirement living standard, meanwhile, now costs a single person £14,400 a year, an increase of 12% versus £12,800 a year ago

Couples who can pool resources should be able to attain living standards at a lower cost per person

The research also found that women’s pension assets less than two-thirds (62%) of men’s by their late 50s. To bridge the gender pension gap women would need to contribute for an additional 19 years or at a 6% higher rate than men. The gender pay gap plus different working patterns are partly to blame for the gender pensions gap.

Professor Matt Padley, Co-director of the Centre for Research in Social Policy at Loughborough University, said “Expectations about living standards in retirement continue to change in subtle ways. The research sets out public consensus about these different living standards with the aim of helping people think in more concrete ways about what they want their own retirement to look like. Their personal retirement goals will be shaped by their own circumstances, needs and preferences.”

“In this year’s findings we see the strong effects of rising prices in what’s needed to meet the cost of food and energy. Following the Covid pandemic, this latest research highlights a pronounced need and enthusiasm among the public for shared experiences beyond the confines of their homes, including activities like eating out and holidays.”

Nigel Peaple, Director Policy & Advocacy, PLSA, said “The cost-of-living has put enormous pressure on household finances over the last year and, as the research shows, this is no different for retirees.

“It’s important for workers saving for retirement to remember the standards are not prescriptive targets, they are a tool to help you engage with the type of spending you think you will do in retirement and to help you plan for it.

“It is also worth highlighting that a couple who each has a full entitlement to the State Pension will achieve the Minimum level, and if each is paid average earnings throughout their working life, they have a good chance of enjoying many aspects of the Moderate living standard. Working and saving is likely to vary over a lifetime, for example taking time off to have children, so it is important to adapt workplace pension contributions to make up for periods not saving.

“Many pension providers now provide tools and calculators on their online platforms to allow savers to pick-and-mix elements of each Retirement Living Standard, allowing them to leave out the things they don’t see as part of their life and tailor the Standards to their individual circumstances and preferences.”

Commenting on the findings, Helen Morrissey, Head of Retirement Analysis at Hargreaves Lansdown said “Our pensions are under pressure as the cost of retirement continues to soar. The cost of a moderate retirement income has grown by an astonishing £8,000 per year for a single person.

“There are several reasons for this – increased food and energy costs are a big factor, but they also reflect people’s changing needs in retirement. The pandemic period took us away from our family and friends, and this experience means time with loved ones and enjoying holidays have become increasingly important to retirees.

“It’s worth emphasising that these are not prescriptive numbers – everyone’s view of what makes for a good retirement is different, and so your income needs could well differ from these figures.

“However, it does show the huge challenges we face in saving for retirement. First is the role of the state pension. This forms the very bedrock of our retirement income. A couple where both partners get the full amount will hit the minimum income standard for retirement before their other pensions come into play. This is an enormous boost, but state pension age is under pressure with recent reports saying it may need to hit age 71 in the near future. This has a massive impact on how much we need to save. This is particularly the case for single people, who are unable to share living costs as a couple would. It is vital that we have a review of the state pension system to make sure it remains sustainable long-term.

“Secondly, it also shows the importance of developing auto-enrolment to help people build decent pensions. Most notably we need to see a timetable for the Auto-enrolment Extension Bill to be implemented, which will bring down the age people qualify, and boost the portion of their income they pay contributions on, and so has the potential to help people contribute more into their pension for longer and really build their financial resilience.”