Mortgage rates have risen significantly since the start of the war in Iran, leaving homeowners facing steep increases in monthly payments – at a time when living costs are already rising across the board, warns Sprive.

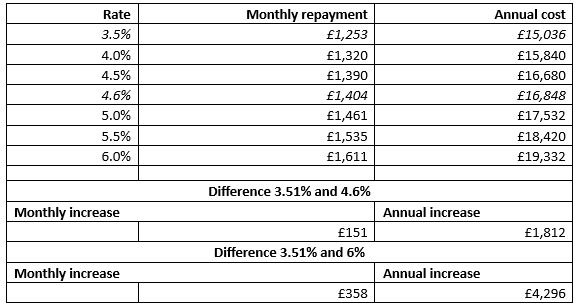

According to Moneyfacts, the lowest available 2-year fixed deal before the start of the conflict in the Middle East was 3.51%, whereas it has now jumped to 4.6%. That equates to an increase of £151 a month, or £1,812 a year. And that is on the lowest possible rate; average rates are now around 5%, with many lenders announcing increases this week to more than 6%, leaving homeowners as much as £4,300 worse off annually.

Jinesh Vohra, CEO of Sprive said “The jump in rates in just a few weeks shows how quickly global events can ripple through the mortgage market and expose homeowners to higher costs,” he said. “With rates going past 5% last week and now many creeping over 6%, the impact is immediate for those looking to buy, remortgage, or sell.

“When markets react like this, lenders often pull back or tighten criteria, leaving borrowers with fewer options almost overnight. Homeowners need to act proactively: review their deals early, lock in fixed rates where possible, and overpay if they can to reduce interest costs.

“In a market like this, homeowners who stay proactive are the ones who benefit most. Tools like Sprive can help by monitoring the market daily for the best mortgage deals, calculating exactly when it makes financial sense for each user to remortgage, and allowing homeowners to chip away at their mortgage using cashback from everyday spending — helping them build resilience against rising costs without making drastic lifestyle changes.”